Economists in the 1920s Thought They Could Not Only Eliminate the Business Cycle But Also Forecast the Future

Bruce Caldwell, the editor of F. A. Hayek's book Contra Keynes and Cambridge: Essays, Correspondence, made two interesting comments in his introductory essay that I am going to expound upon in this article because these two comments nicely highlight my blog's theme regarding the ignorance of the experts.

The Expert Forecasters Failed to Predict the Great Depression

According to Robert Leonard, by the late 1920s business cycle research fell into two major school of thought. The Austrian School of Economics — the school of economic thought that Hayek belonged to at this time — rejected both of the schools of thought mentioned by Leonard. The reason why I select this quote from Leonard is because I want to establish what the experts in the field were saying prior to the Great Depression:

By the late 1920s, the most prominent contributions to the study of the cycle fell into two groups: the attempts by Henry Ludwell Moore, like Jevons before him, to show the existence of a periodic economic cycle generated by noneconomic forces, and the empirical work by both Mitchell, at the National Bureau of Economic Research, and Persons and Bullock, constructing the business barometers at Harvard's Committee for Economic Research.¹

To further emphasize my primary point that I am discussing the forecasting experts of the 1920s, I am going to cite from Walter A. Friedman's book. In Friedman's book, he makes this point abundantly clear:

More than any of the other forecasters profiled in this book, the Harvard team celebrated the idea of using the world's most elite institutions and most creative minds to solve the problem of forecasting. By doing so, they hoped to wrest the field away from entrepreneurs like Roger Babson and John Moody. In 1929, the renowned Harvard economist Frank W. Taussig (1859-1940) said of the Harvard Economic Service: "Nothing of this sort — the application of the highest scholarship under academic auspices to the perplexing oscillations and irregularities of modern trade and industry — had ever been tried before."²

But unfortunately, things did not work out for the forecasting experts at Harvard. This particular problem was noted by Hayek scholar Bruce Caldwell. The basic problem for the Harvard Economic Service was simply that they failed to predict the Great Depression:

Hayek spent some of his stay in the United States learning about economic forecasting. It was a popular new topic at the time, with institutes like the Harvard Economic Service (which regularly published a set of 'economic barometers' on the state of the economy) springing up everywhere. (Most of these institutes died out after failing to foresee the coming Depression).³

The Experts Thought That They Could Eliminate the Business Cycle

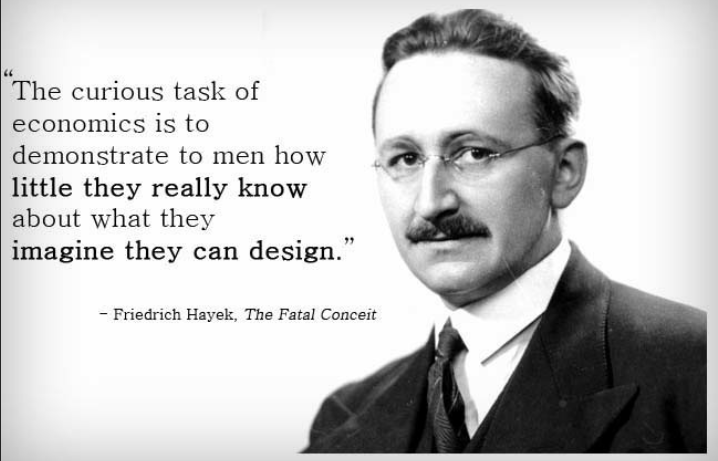

By the 1920s, some economists thought that they could eliminate the business cycle by adopting a policy of general price level stabilization. To implement this policy, economists recommended the use of open market operations. What I find interesting is that Hayek's replies were always the same; namely, he argued that the experts would not have enough knowledge or enough information to do what they wanted to do. In other words, their ignorance would prevent them from successfully eliminating the business cycle and would prevent them from successfully stabilizing the general price level.

First, let me cite professor Hayek's reaction to the idea that economists, using the Federal Reserve System, should try to eliminate the business cycle:

The Federal Reserve System had been established in 1913 in the hope that centralized cash reserves might help mitigate financial panics of the types that had plagued the American economy in previous decades. By the 1920s, certain American economists had more ambitious goals: not merely to counteract crises already under way, but "to prevent cyclical and crisis phenomena from evidencing themselves at all." Hayek thought that this was too ambitious an aim. Though it might be possible to restrict the cycle to narrower bounds than before, achieving its total elimination required more knowledge than then existed or might ever exist.⁴

More specifically, the proposed solution to the business cycle involved stabilizing the general price level using open market operations. Caldwell writes that

the burning question of the day for the American economics profession was a characteristically pragmatic one: What actions if taken by the central monetary authority hold the best chance of eliminating the cycle? Though different schemes were offered, stabilization of the general price level emerged as the favoured policy. If the price level (as measured by a statistically constructed index number) rose beyond a certain point, the Federal Reserve would raise the discount rate (and possibly also sell bonds in the open market to reduce the amount of currency outstanding; such "open market operations" were then still controversial in the United States) in an effort to slow economic activity. If the price level fell, the opposite procedure would be followed.⁵

I think it is really interesting that Caldwell describes open market operations in the 1920s as a controversial policy proposal. When I took first year undergraduate macroeconomics in the year 2000, open market operations were presented as nothing controversial. They were simply presented as "the way it is."

However, when I went snooping around in some of my other books on the history of economics in the 1920s, I did find confirmation of Caldwell's assertion about the controversial nature of using open market operations. According to Benjamin M. Anderson, the use of open market operations to finance the stock market boom of the 1920s was a breach of orthodox central bank policy:

The Federal Reserve Act would have worked well had traditional central bank policies been followed, namely: the holding of the rediscount rate above the market rates, and the use of open market operations primarily as an instrumentality for tightening the money market, not for relaxing it.

The Federal Reserve System was created to finance a crisis and to finance seasonal needs for pocket cash. It was not created for the purpose of financing a boom, least of all for financing a stock market boom. But from early 1924 down to the spring of 1928 it was used to finance a boom and used to finance a stock market boom.⁶

Returning back to Hayek and the question of eliminating business cycles by stabilizing the general price level, I want to point out that Hayek replied again by pointing out the ignorance of the experts. In this case, he argued that the experts will be looking at the general price level for information about what to do, but they will not find that information there. Instead, to find the necessary information, they need to be looking at the behaviour of the relative prices of different commodities:

The objection that appears to us to be much more serious is that the cyclical movement finds its initial expression not in the behaviour of the general price level but in that of the relative prices of the individual groups of commodities. Hence an index of the general price level cannot yield any relevant information as to the course of the cycle nor more importantly can it do so at the right time.⁷

Concluding Remarks

One major point I hope you saw is that even the best of the best — in this particular case the expert forecasters at the Harvard Economic Service — made mistakes. They failed to predict the Great Depression, and a failure of this magnitude means that adopting the decision rule that says "just trust me, I'm the expert" is potentially dangerous to the consumer of expert advice. Expert advice is obviously not a sure thing.

The second point I hope you saw is that experts, even with the best of intentions, — in this particular case, the intention of solving business cycles — had a tendency to overestimate the amount of knowledge they actually had. Consequently, as a consumer or user of expert advice, the lesson learned here is to approach the expert like a data sufficiency question on the GMAT exam,⁸ i.e., does the expert really have enough information and enough knowledge to come to the conclusions that he or she is coming to?

Footnotes

¹ Robert Leonard, Von Neumann, Morgenstern, and the Creation of Game Theory: From Chess to Social Science, 1900-1960, Historical Perspectives on Modern Economics (New York: Cambridge University Press, 2010), 96.

² Walter A. Friedman, Fortune Tellers: The Story of America's First Economic Forecasters (Princeton: Princeton University Press, 2014), 130-131.

³ Bruce Caldwell, ed., editor’s introduction to The Collected Works of F. A. Hayek, vol. 9, Contra Keynes and Cambridge: Essays, Correspondence, by F. A. Hayek (Indianapolis: Liberty Fund, 1995), 11.

⁴ Caldwell, ed., Contra Keynes and Cambridge, 12.

⁵ Caldwell, ed., Contra Keynes and Cambridge, 13.

⁶ Benjamin M. Anderson, Economics and the Public Welfare: Financial and Economic History of the United States, 1914-1946 (1949; repr., Princeton: D. Van Nostrand Company, 1965), 136.

⁷ Caldwell, ed., Contra Keynes and Cambridge, 13.

⁸ GMAT stands for the Graduate Management Admission Test. It is the standardized test used by business schools to help them decide who to admit to a Master of Business Administration (MBA) program.